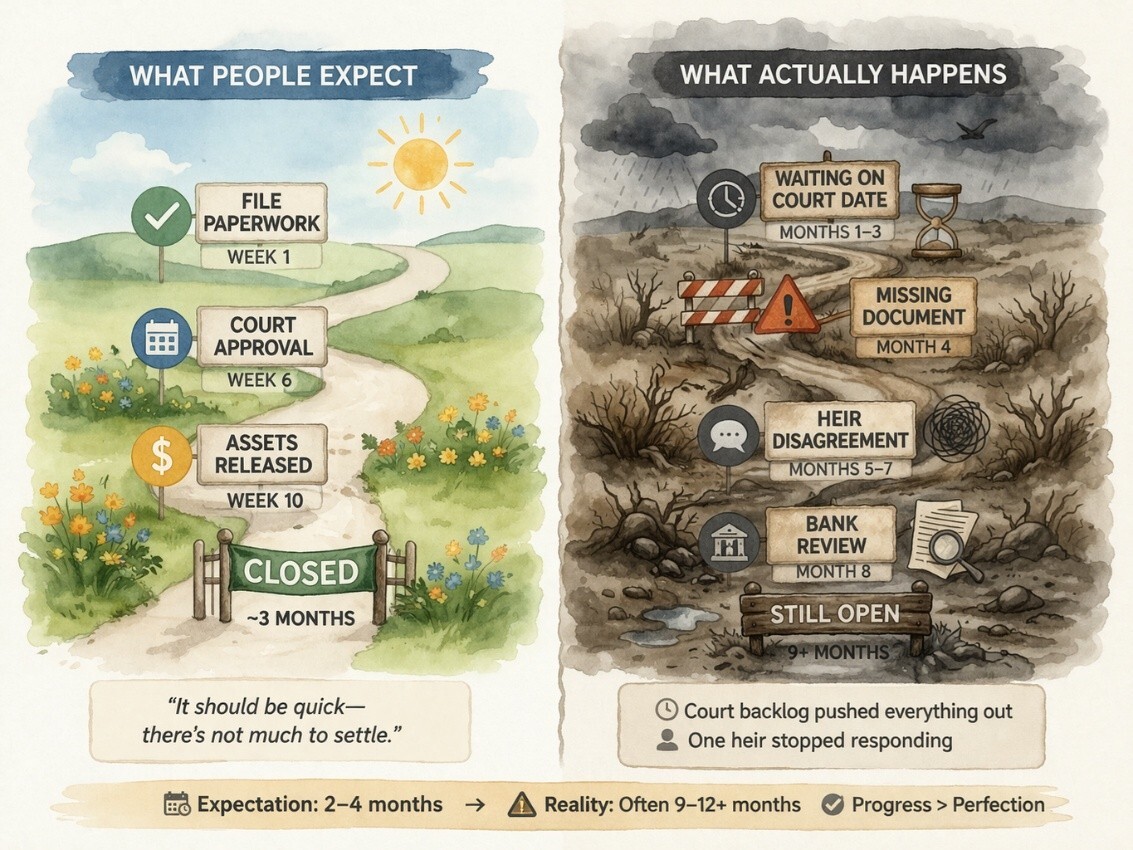

Most probate and guardianship bonds are simple. A few signatures, a quick check of the order, a clean Fiduciary, and everything moves fast.

But every attorney eventually hits a case where things don’t go that way. The bond stalls. The questions pile up. The Fiduciary gets nervous. The court grows impatient. Your paralegal keeps refreshing their inbox.

From the outside, this can feel unpredictable. From the inside, there are very specific reasons why certain bonds take longer or require more care.

These are the key factors I’ve seen in thousands of cases, the ones that determine whether a bond is straightforward… or becomes one of those files that keeps everyone on edge.

Let’s walk through the most common issues together.

1. Credit Is About Risk

Credit is by far the biggest variable because the Surety is guaranteeing the Fiduciary’s honesty and financial responsibility to the court.

In practice, this means someone with excellent credit moves through smoothly. But someone with lower credit, a thin file, or past financial trouble may raise flags enough that the Surety wants to understand the story behind the numbers.

I always remind attorneys: most Fiduciaries aren’t trying to hide anything. They just don’t realize how much their credit affects the process until the bond becomes urgent. Helping them understand this early reduces embarrassment and speeds up approvals later.

2. Indemnity Can Surprise People

Every bond requires the Fiduciary to sign an indemnity agreement. To us, this is standard. To them, it can feel intimidating. It basically says: “If the Surety pays out a loss because of something you did, you agree to reimburse them.”

The problem?

People sometimes hesitate. They want a family member to review it. Or they stop returning calls. Or they say, “Let me think about it,” right when the judge needs the bond today.

If you can prepare your clients early, before emotions run high, indemnity becomes a routine part of the process instead of a roadblock.

3. Low Credit Doesn’t Mean ‘No’ But It Does Change the Path

There are several workarounds when the Fiduciary doesn’t meet the initial credit threshold.

Sometimes you can use a restricted deposit. Sometimes, a Co-Fiduciary with stronger credit can step in. Sometimes the client can provide additional documentation that answers the underwriter’s concerns. Sometimes the court will simply reduce exposure by restricting certain funds.

It’s rarely about disqualifying someone. It’s about making sure the Fiduciary is supported with safeguards that protect the Ward, the estate, and the Beneficiaries. Because at the end of the day, a bond exists to protect people who can’t protect themselves.

4. Collateral Is Rare, But It Happens

Collateral is the last resort, usually in high-value estates where:

- There’s a lot of illiquid property

- There’s internal conflict

- The Fiduciary has severe credit issues

- Or the estate involves complex or risky assets

Most clients freeze when they hear “collateral,” so preparing them early is helpful. It’s not common, but when it does come up, it’s almost always because the Surety needs confidence that significant assets are protected.

Think of it as the Surety saying, “We’re willing to help, but we need to be sure everyone is safe.”

5. Red Flags Aren’t Dealbreakers But The Do Slow Things Down

We see patterns.

- A Fiduciary who lives out of state.

- A previous late accounting in another case.

- An estate full of family conflict.

- A Guardian who has never managed money before.

- A recently filed divorce.

- A Beneficiary who has already objected to everything.

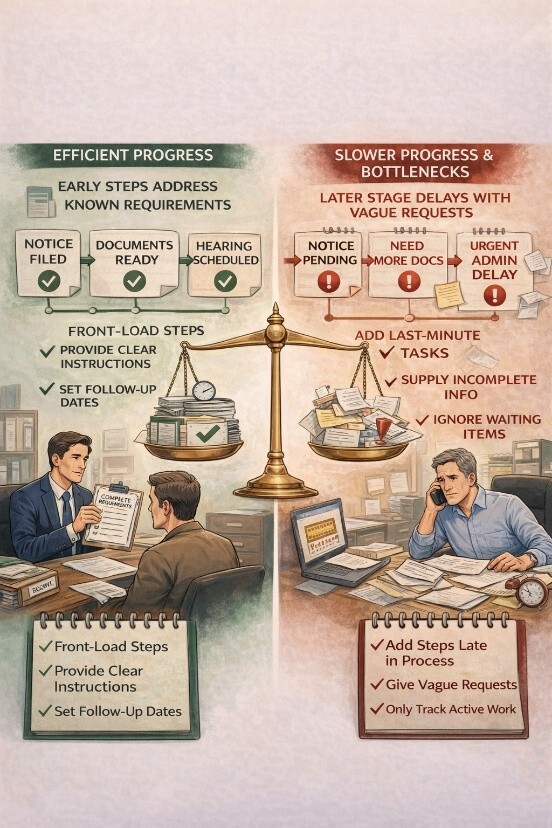

None of these things stop a bond from being issued, but they do require clarity. Sometimes a single sentence of context solves the whole problem. Other times, it just means the underwriter needs a little time to understand what’s really going on. The more context we have, the faster we can move.

6. Courts Don’t Always Use the Same Formula

This is especially true in probate.

Guardianship statutes are clear: dollar-for-dollar bond or restricted accounts.

Straightforward.

Probate?

Completely different.

There is no statute, so each judge relies on their experience and comfort level. One judge may treat real property as if it’s liquid. Another may ignore it entirely. One may include annual income. Another doesn’t. One may require supplemental bonding if assets change. Another waits for the inventory.

Knowing this ahead of time helps attorneys prevent last-minute surprises in court.

When a bond is easy, it’s invisible; it just happens. When a bond is hard, it becomes the center of the case. Clients panic. Paralegals get frustrated. The judge wants answers. And everyone looks to you.

Understanding the “why” behind difficult approvals arms you with the confidence to guide your clients calmly and accurately, even when the case is complicated. And if you ever run into a situation where you’re unsure how the court or the Surety will respond, my team and I are here to be a sounding board.

Sometimes the fastest way to fix a hard case is simply knowing what the issue really is. If you need a bond now or want clarity on an unusual situation, you can always count on us.

Call 800-828-2226 or Click Here.

To your success,

Darren Vermost

The Bond Guy

and the Probate Bond Pros Team